The Future of Impact: Beyond $1 Billion Catalyzed

From Fringe to Force: The New Era of Impact Investing

Like the rest of us, impact investing has come a long way over the past two decades, when faith-based groups and mission-driven pioneers were experimenting in a fragmented ecosystem with few tools and little data. What began as a niche practice is now a global movement, with more than $1.5 trillion in impact assets under management and growing demand from institutions, families, and advisors alike. And like any growing pains, the field’s expansion has also exposed some common challenges in impact investing: misaligned metrics, limited access to private markets, and a gap between purpose and execution.

As a firm built to solve many of those pain points, we’ve seen the evolution of impact investing up close and personal. As CapShift has recently surpassed $1 billion mobilized into impact investments by our community to date, we offer a look behind the curtain on the impact sectors that have seen the most success, where the market is headed—and what it means for the future of impact.

Drawing on data from our Research Engine of over 1,400 impact opportunities and insights from leading allocators, we share some of the trends, tools, and themes that are reshaping portfolios today and setting the course for our next billion dollars allocated.

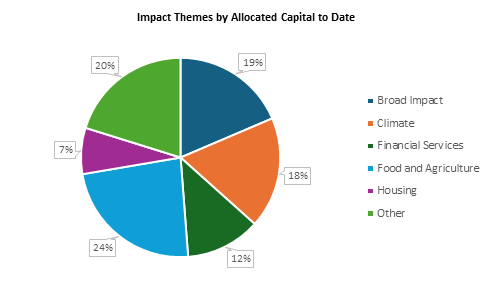

Sector Spotlight: Where is Capital Moving?

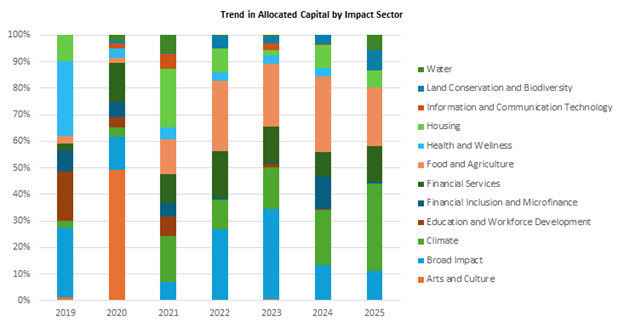

Over the past five years, CapShift’s clients have allocated funds across impact areas spanning all 17 United Nations Sustainable Development Goals, including housing, financial services, and health–but certain impact areas have shown greater popularity and staying power. Across all impact areas, Food and Agriculture, Climate, and Broad Impact represent over 60% of capital allocated by CapShift’s clients.

![]()

Climate

Urgency around decarbonization, resilient infrastructure, and technological innovation is driving sustained investor engagement in climate. According to Morgan Stanley’s Sustainable Signals, nearly 90% of individual investors are interested in sustainable investing, with over 80% identifying the clean energy transition as a viable path to generating returns. This reflects a broader redefinition of climate from a risk to be mitigated into a strategic growth opportunity.

At CapShift, we‘ve seen this shift translate directly to dollars moved. Since 2021, climate has been one of the top sectors, both in terms of number of transactions and capital allocated. While early allocations were primarily catalytic through recoverable grants, recent years marked a shift toward private equity and debt. This evolution has prompted a closer look at why private equity and venture capital have become such central channels for deploying climate capital.

Investors are increasingly seeing private equity and venture capital as avenues to access climate innovation and resilience. Private equity has become a preferred vehicle for adaptation-focused strategies that require long-term capital and active governance — such as grid modernization, water systems, and resilient infrastructure. BCG estimates that the global adaptation and resilience market could reach $0.5-$1.3 trillion annually by 2030, pointing to both market demand and financial opportunity. Institutional investors are also drawn to the structure and discipline of fund models, which offer oversight, ESG integration, and exit planning. On the venture side, declining costs in renewables, batteries, and sensors have improved margins and commercial viability.

Over half of all climate investments by CapShift’s clients in the last year have taken the form of private direct investments, reflecting a move away from pooled funds toward higher-conviction, theme-specific opportunities. This trend is driven by investors seeking more control and transparency, greater alignment with net zero goals, and direct exposure to innovation in areas like renewable energy, sustainable materials, and climate adaptation. Direct equity deals enable investors to target scalable infrastructure and early-stage climate solutions. This approach reflects a broader shift from defensive ESG positioning toward proactive, high-conviction strategies.

Among family offices, this trend is especially evident. According to the UBS Global Family Office Report, 48% cite climate change as a risk to their financial objectives over the next five years, and over a third are already allocating to investments in areas such as clean technology and sustainability. These choices reflect a growing preference for mission-aligned strategies that offer both thematic focus and greater control over capital deployment.

Food and Agriculture

Food and agriculture has emerged as a core strategy for investors seeking both portfolio resilience and real-world systems change. Across our client base, CapShift has seen a high growth rate in food and agriculture investments since 2019,which reflects rising investor recognition that food systems are central to addressing climate risk and social inequity. These investments are increasingly viewed as durable, real-economy assets—tied to land, storage, and supply infrastructure—that offer inflation protection, low market correlation, and local, measurable impact. This corresponds with broader market sentiment: Morgan Stanley finds North American investors ranking improved food security among their top investment outcomes and the GIIN ranks food and agriculture as the sector with the most growth potential behind energy, with 61% of investors planning to increase exposure.

Structurally, the sector is dominated by private debt, commanding 62% of CapShift’s total food and agriculture allocations since 2022. The asset class is attractive due to its stable returns, while offering support for small and mid-sized operators, blended finance compatibility, and flexibility to align capital with short-term impact outcomes.

Broad Impact

Broad impact strategies are now among the top three allocation categories among CapShift’s clients. These strategies offer exposure across multiple themes such as gender equity, healthcare, education, and financial inclusion. More than 80% of capital in this segment has been deployed through private debt funds, which investors value for their scale, professional management, and streamlined execution. These strategies are increasingly being used as core building blocks within portfolios.

With broad impact strategies, allocators are not only seeking diversification but also mission-aligned options that balance flexibility with measurable results. This approach is particularly attractive to family offices with multi-generational goals, donor-advised funds aiming for simplified deployment, and advisors who want diligence-ready solutions. One example of a broad impact strategy is a private credit fund providing loans to small and mid-sized enterprises in emerging markets across sectors like clean energy, healthcare, and financial services. With support from foundations providing first-loss capital, the fund combines thematic breadth with reduced risk and greater income-generating potential. Such funds illustrate how broad impact strategies can deliver real-world outcomes while meeting portfolio needs.

Looking Ahead: Four Trends in Impact by 2030

As impact investing matures, it is growing into a more structured and strategic discipline. Regulatory initiatives like the Sustainable Finance Disclosure Regulation and the Taskforce on Nature-related Financial Disclosures (TNFD) are driving more transparency and thematic rigor. Climate urgency and social mobilization is fuel for purpose. The field is entering an era of systems-level thinking and institutional sophistication. Below are four key trends poised to define impact investing by 2030:

Nature-Based Solutions and Biodiversity

Why it is gaining traction:

Financial markets are recognizing that nature loss is a systemic risk that can erode long-term value. Biodiversity degradation disrupts global supply chains, reduces agricultural output, increases insurance liabilities, and magnifies exposure to climate volatility. Investors are also responding to new frameworks like TNFD, which formalizes nature risk into portfolio-level disclosures. This shift is visible to us at CapShift, as we’ve seen client allocations to nature-based solutions grow at a compound annual growth rate of 73% since 2020. Globally, the GIIN reports a 64% increase in allocations toward SDG 15: Life on Land, during the same period, reflecting rising appetite for ecological outcomes that go beyond carbon.

How it is showing up:

Examples of this shift include a recoverable grant model that provides capital to protect working forests while recycling funds through resale or easements. One firm supports regenerative farmers through long-term, sustainability-linked leases that support soil health and local food systems. Meanwhile, another fund redirects tech and venture capital gains into permanent conservation via nonprofit land trusts, integrating biodiversity into modern wealth planning. These different approaches illustrate ways that investors are aligning long-term ecological stability with capital stewardship.

Why it matters: Nature-focused investments help reduce long-term ecological and financial risks while aligning with emerging regulatory frameworks like TNFD. They provide access to real assets with measurable environmental outcomes and offer a proactive way to manage portfolio exposure to systemic nature-related risks.

Housing and Social Infrastructure

Why it is gaining traction:

Affordable housing has emerged as a core impact priority, driven by intersecting crises in affordability, climate change, and racial equity. Housing is now viewed as a durable real asset that can deliver consistent cash flow while meeting deep community needs. For investors, it offers measurable social returns, eligibility for tax incentives, and strong resilience to inflation. CapShift’s data shows allocations to housing have stabilized at elevated levels since 2023, reflecting allocator conviction in the sector. As noted in CapShift’s article on housing, investors are increasingly turning to housing as a multi-dimensional strategy that advances equity, environmental sustainability, and long-term value.

How it is showing up:

Recent investment examples highlight this intersection of impact and return. One fund has raised over $100 million to support affordable housing, early learning centers, and healthcare facilities in underserved communities, while delivering fixed-income returns. Another has mobilized over $50 million to retrofit low-income housing with energy-efficient upgrades, reducing both carbon emissions and utility costs.

Why it matters: Affordable housing and community infrastructure offer inflation-protected income and real asset exposure, with the added benefit of addressing persistent social gaps. These investments combine measurable community outcomes with long-term portfolio stability and growing policy support.

Climate Adaptation

Why it is gaining traction:

As the frequency and severity of floods, wildfires, droughts, and other climate shocks rise, investors are recognizing adaptation as essential to both financial risk management and impact strategy. Governments and multilaterals are co-investing in resilient infrastructure, enabling blended financing models. In tandem, disclosure frameworks are pushing investors to incorporate physical risk into portfolio assessments. The Financial Times reports a growing flow of capital into adaptation–linked asset classes such as flood-proof housing and resilient water systems. CapShift is also observing meaningful upticks in client interest across strategies that prioritize place-based resilience.

How it is showing up:

Recent innovations in climate risk finance highlight how investors can align returns with resilience. In 2025, catastrophe bond issuance reached a record $18 billion, as insurers transferred defined risks like wildfires and hurricanes to capital markets. These bonds deliver double digit yields, offering asset allocators diversification while supporting rapid climate response. One fund has used parametric insurance to provide over $170 million in payouts for droughts and floods over the past decade, covering more than 50 million people across multiple African countries.

Why it matters: Adaptation-linked investments offer downside protection against physical climate risks while delivering uncorrelated returns. With rising demand for resilient infrastructure and new financial instruments like catastrophe bonds gaining traction, adaptation is becoming a practical component of institutional risk management.

Blended Finance

Why it is gaining traction:

Blended finance is increasingly attractive for allocators seeking to move capital into sectors and regions that remain underserved due to perceived risk or complexity. By combining philanthropic or public capital with private investment, these structures reduce downside exposure and enable large-scale participation. Blended models are especially well suited for family offices, DAFs and foundations that want to catalyze impact without compromising return potential. According to Convergence, over 1,350 blended deals have mobilized more than $249 billion highlighting the growing institutional appeal of tiered capital structures.

How it is showing up:

One state-sponsored fund blends public capital with private sector financing to accelerate clean energy deployment. In fiscal year 2023–2024, it committed over $336 million across 16 transactions and has catalyzed over $2.3 billion in total investments. Similarly, a regenerative agriculture fund in the U.S. combines philanthropic first-loss capital with senior preferred tranches to offer flexible, non-extractive loans to farmers often excluded from traditional credit. These funds demonstrate how blended finance is unlocking scale and reducing perceived risk across climate and food systems.

Why it matters: Blended finance creates entry points into high-impact sectors by reducing downside risk and attracting more capital into underserved markets. These structures help investors achieve thematic goals—such as climate, food systems, or inclusion—while maintaining return potential and portfolio discipline.

Closing the Gap: From Purpose to Execution

Impact investing is transitioning from general objectives to more targeted implementation. As climate, environmental, and social risks gain financial significance, investors are adopting structured, outcome-based strategies. Success will depend on aligning capital with specific goals. Nature-based solutions require long-term, place-based models. Housing and social infrastructure call for measurable community outcomes. Adaptation and blended finance offer scalable, risk-managed entry points into underserved sectors.

The field is heading toward more precision and accountability—and the portfolios that stand out will be the ones that match purpose with follow-through.

The next chapter of impact investing won’t be defined by just how much capital is committed. It will be defined by what that capital builds.

About the Authors

Garima Gupta is a Manager of Impact Investments at CapShift. She collaborates with the investment research team and advisory practice to identify and assess investment opportunities aligned with social and environmental impact goals. Prior to joining CapShift, Garima practiced law in India. She holds a Master of International Business from The Fletcher School at Tufts University with a concentration in social finance.

Amir Bajwa is an Impact Investment Fellow at CapShift, where he contributes to research and analysis across a range of impact investment opportunities. He is passionate about mobilizing capital to accelerate the transition to resilient, low-carbon economies. Amir is currently pursuing a Master of Public Administration at Columbia University. Prior to CapShift, he worked in microfinance and impact investing, with a focus on building climate adaptation solutions for underserved communities.