“When COVID started, we were told not to come back until further notice,” Mary told me. She was talking about the textile factory where she worked before the pandemic hit. I had bumped into Mary during a trip home to Guatemala — in a waiting room — and struck up a conversation about how the pandemic impacted her and her family.

Mary told me that she couldn’t afford to wait for a call back. Even before the pandemic, she was expending her earnings on a daily basis to provide for her 3 children and 2 grandchildren. “I live and earn my money day-by-day,” she had said. The uncertainty of the pandemic threatened to throw that already precarious balance into disarray.

Fortunately, Mary found a lifeline: A friend introduced her to a cooperative — an organization that provides loans, training, and resources to entrepreneurs — in her neighborhood, and she learned that starting a small business with a loan was an option for her. Now, Mary runs a small catering operation with her daughters, preparing and delivering food for events. “My daughters and I work together, and our income increased. I paid the loan back in 3 months, with payments every two weeks” she told me. “The cooperative helped me with planning. Without that help, I would still be waiting on the textile factory to call me back.”

Mary’s situation wasn’t unique. As the pandemic unfolded around the world, women bore the brunt of its economic effects. In fact, the United Nations Conference on Trade and Development estimates that the economic aftermath of the pandemic threatens four decades of hard-won progress on the fight for gender equality.

Microfinance institutions that serve women in rural areas are especially critical in this moment as the global health crisis jeopardizes the livelihoods and economic opportunity of millions of women around the world. But at a time when they’re most needed, they’re facing their own crisis.

Here’s why.

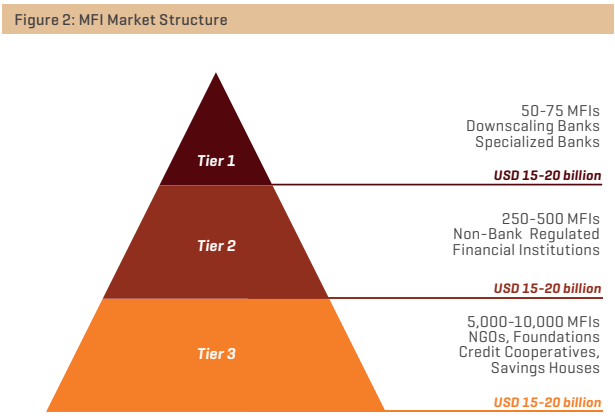

When people hear the words “microfinance institution,” the image that typically jumps to mind is a large, multinational organization like Grameen Bank or Finca International. Backed by large institutional asset owners and multilateral development banks, these establishments operate at scale and have a national — or international — reach. Left in the shadow of these microfinance giants, however, are peers more modest in size and reputation — establishments like the cooperative in Mary’s neighborhood. They are commonly referred to as “Tier 2” and “Tier 3” institutions by the industry, and are primarily comprised of non-banking institutions, such as NGOs, cooperatives, and saving houses. While the scale of each of these organizations is smaller, the number of borrowers they serve and the money they move into developing economies are not. In fact, these institutions reach approximately two-thirds of the entire microfinance market.

Source: Roland Dominicé, Symbiotics. “Microfinance Investments.” p. 20

However, unlike their “Tier 1” counterparts that operate at scale, these Tier 2 & 3 institutions depend more heavily on specialized lenders and philanthropic capital from donors to carry out their mission. And when the pandemic hit, these institutions felt the pressure of a double bind: On the funding side, smaller institutions are projected to face greater challenges negotiating with lenders and funders than larger Tier 1 institutions; in terms of lending operations, a large number of borrowers restructured their loans, generating a liquidity issue for many smaller microfinance institutions. This perfect storm presented a potentially dire solvency challenge for many Tier 2 and 3 institutions — leaving them unable to serve their most vulnerable constituents, rural women like Mary, at their time of greatest need.

Charitable asset owners have the opportunity to make a difference at this critical juncture. Mobilizing impact dollars to Tier 2 & 3 microfinance institutions may aid in their goals of facilitating economic recovery in rural areas, empowering women through financial independence and economic opportunities, increasing access to benefits, and supporting families in emerging markets. Donors have the ability to help transform these communities with their capital — and help foster economic opportunity for the people like Mary through the thousands of Tier 2 & 3 microfinance institutions in developing economies around the world.